Financialization of an economy

This is an excerpt from "Bitcoin is the great definancialization" by Parker Lewis. Here he discusses the misalignment of incentives and excessive risk-taking that arises when people are confronted with a guaranteed loss of savings.

This is an excerpt from a larger essay named Bitcoin is the Great Definancialization by Parker Lewis.

Have you ever had a financial advisor (or maybe even a parent) tell you that you need to make your money grow? This idea has been so hardwired in the minds of hard-working people all over the world that it has become practically second nature to the very idea of work.

The line has been repeated so many times that it is now a de facto part of working culture. Get a salaried position, max out your 401-K contribution (maybe your employer matches 3%!), select a few mutual funds with catchy marketing names and watch your money grow. Most folks navigate this path every two weeks on auto-pilot, never questioning the wisdom nor being conscious of the risks. It is just what “smart people” do. Many now associate the activity with savings but in reality, financialization has turned retirement savers into perpetual risk-takers and the consequence is that financial investing has become a second full-time job for many, if not most. Financialization has been so errantly normalized that the lines between saving (not taking risk) and investing (taking risk) have become blurred to the extent that most people think of the two activities as being one in the same. Believing that financial engineering is a necessary path to a happy retirement might lack common sense, but it is the conventional wisdom.

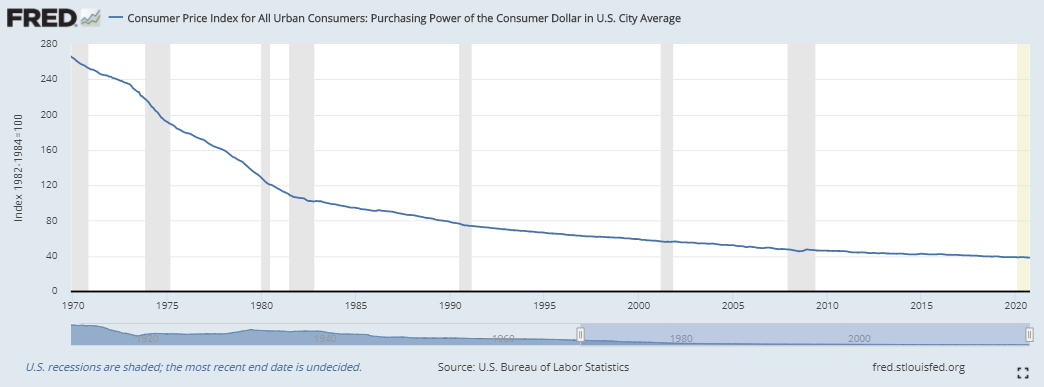

Over the course of the past several decades, economies everywhere, but particularly those in the developed world (and specifically the United States), have become increasingly financialized. Increased financialization has become the necessary companion to the idea that you must make your money grow. But the idea itself — that ‘you must make your money grow’ — only really emerged in the mainstream consciousness as everyone similarly became conditioned to the unfortunate reality that money loses its value over time.

Money Loses Value → Need to Make Money Grow → Need Financial Products to Make Money Grow → Repeat.

The extent to which the need even exists is largely a function of money losing its value over time; that is the starting point, and the most unfortunate part is that central banks intentionally engineer this outcome. Most global central banks target the devaluation of their local currencies by approximately 2% per year and do so by increasing the money supply. How or why is less relevant; it is a reality and there are consequences. Rather than simply being able to save for a rainy day, future retirement funds are invested and put at constant risk, often just as a means to keep up with the very inflation manufactured by central banks.

The demand function is perversely driven by central banks devaluing money to induce such investments. An over financialized economy is the logical conclusion of monetary inflation, and it has induced perpetual risk taking while disincentivizing savings. A system which disincentivizes saving and forces people into a position of risk taking creates instability, and it is neither productive nor sustainable. It should be obvious to even the untrained eye, but the overarching force driving the trend toward financialization and financial engineering more broadly is the broken incentive structure of the monetary medium which underpins all economic activity.

At a fundamental level, there is nothing inherently wrong with joint-stock companies, bond offerings, or any pooled investment vehicle for that matter. While individual investment vehicles may be structurally flawed, there can be (and often is) value created through pooled investment vehicles and capital allocation functions. Pooled risk isn’t the issue, nor is the existence of financial assets. Instead, the fundamental problem is the degree to which the economy has become financialized, and that it is increasingly an unintended consequence of otherwise rational responses to a broken and manipulated monetary structure.

What happens when hundreds of millions of market participants come to understand that their money is artificially, yet intentionally, engineered to lose 2% of its value every year? It is either accept the inevitable decay or try to keep up with inflation by taking incremental risk. And what does that mean? Money must be invested, meaning it must be put at risk of loss. Because monetary debasement never abates, this cycle persists. Essentially, people take risk through their “day” jobs and then are trained to put any money they do manage to save at risk, just to keep up with inflation, if nothing more. It is the definition of a hamster wheel. Run hard just to stay in the same place. It may be insane but it is the present reality. And it is not without consequence.

Savings vs. Risk

While the relationship between savings and risk is often misunderstood, risk must be taken in order for any individual to accumulate savings in the first place. Risk comes in the form of investing time and energy in some pursuit that others value (and must continue to value) in order to be paid (and continue to be paid). It starts with education, training and ultimately perfecting a craft over time that others value.

That is risk taking. Investing time and energy in an attempt to earn a living and to produce value for others, while also implicitly accepting high degrees of future uncertainty. If successful, it ends with a classroom of students, a product on a shelf, a world-class performance, a full day of hard manual labor or anything else that others value. The risk is taken on the front end with the hope and expectation that someone else will compensate you for your time spent and value delivered. Compensation typically comes in the form of money because money, as an economic good, allows individuals to convert their own value into a wide range of value created by others. In a world in which money is not manipulated, monetary savings would best be described as the difference between the value one has produced for others and the value one has consumed from others. Savings is simply consumption or investment deferred into the future; or said another way, it represents the excess of what one has produced but not yet consumed. That however is not the world that exists today. With modern money, there is a fly in the ointment.

Central banks create more and more money which causes savings to be perpetually devalued. The entire incentive structure of money is manipulated, including the integrity of the scorecard that tracks who has created and consumed what value. Value created today is ensured to purchase less in the future as central banks allocate more units of the currency arbitrarily. Money is intended to store value, not lose value and with monetary economics engineered by central banks, everyone is unwittingly forced into the position of taking risk as a means to replace savings as it is debased. The unending devaluation of monetary savings forces unwanted and unwarranted risk taking on to those that make up the economy. Rather than simply benefiting from risks already taken, everyone is forced to take incremental risk.

Forcing risk taking on practically all individuals within an economic system is not natural nor is it fundamental to the functioning of an economy. It is the opposite and it is detrimental to the stability of the system as a whole. As an economic function, risk taking itself is productive, necessary, and inevitable. The unhealthy part is specifically when individuals are forced into taking risk as a byproduct of central banks manufacturing money to lose value, whether those taking risk are conscious of the cause and effect or not. Risk taking is productive when it is intentional, voluntary and undertaken in the pursuit of accumulating capital.

While deciphering between productive investment and that which is induced by monetary inflation is inherently grey, you know it when you see it. Productive investment occurs naturally as market participants work to improve their own lives and the lives of those around them. The incentives to take risk in a free market already exist. There is nothing to be gained, and a lot to lose, through central bank intervention.

The operation of risk taking becomes counterproductive when it is borne more out of a hostage taking situation than it is free will. That should be intuitive and it is exactly what occurs when investment is induced by monetary debasement. Recognize that 100% of all future investment (and consumption for that matter) comes from savings. Manipulating monetary incentives, and specifically creating a disincentive to save, merely serves to distort the timing and terms of future investment.

It forces the hand of savers everywhere and unnecessarily lights a shortened fuse on all monetary savings. It inevitably creates a game of hot potatoes, with no one wanting to hold money because it loses value, when the opposite should be true. What kind of investment do you think that world produces? Rather than having a proper incentive to save, the melting ice cube of central bank currency has induced a cycle of perpetual risk taking, whereby the majority of all savings are almost immediately put back at risk and invested in financial assets, either directly by an individual or indirectly by a deposit-taking financial institution. Made worse, the two operations have become so sufficiently confused and conflated that most people consider investments, and particularly those in financial assets, as savings.

Without question, investments (in financial assets or otherwise) are not the equivalent of savings and there is nothing normal or natural about risk taking induced by central banks which create a disincentive to save. Anyone with common sense and real world experience understands that. Even still, it doesn’t change the fact that money loses its value every year (because it does) and the knowledge of that fact very rationally dictates behavior. Everyone has been forced to accept a manufactured dilemma. The idea that you must make your money grow is one of the greatest lies ever told. It isn’t true at all. Central banks have created that false dilemma. The greatest trick that central banks ever pulled was convincing the world that individuals must perpetually take risk just to preserve value already created (and saved). It is insane, and the only practical solution is to find a better form of money which eliminates the negative asymmetry inherent to systemic currency debasement.

Takeaway If people are guaranteed to lose the value of their savings over time due to monetary inflation, they will attempt to protect their wealth with unnatural and uninformed risk taking, creating an unhealthy foundation for an economy.

Last updated